Recent data from the Office for National Statistics reveals that the government has borrowed more than £300 billion so far to shore up Britain’s finances during the coronavirus lockdown.

This is a record amount of borrowing during peacetime and has left many wondering how the government intends to pay for its heightened level of public spending.

One route it might take, according to the Telegraph, could be to reduce the tax benefits you receive on your pension. The paper recently reported Treasury officials are considering several changes that the chancellor may announce in his autumn statement.

Read on to discover how these changes might affect you and how the reforms could reduce the level of growth of your retirement fund.

1. The government could reduce the tax rebate for higher-rate taxpayers

Currently, every pound you contribute to your pension is boosted by the level of Income Tax you pay, thanks to relief from the government.

If you are a basic-rate taxpayer you’ll typically receive an additional 20% on your contributions, which means every £100 pension contribution effectively costs you £80. If you’re a higher-rate taxpayer, you receive 40% relief and, as an additional-rate taxpayer, you’ll have a 45% boost.

This is subject to the Annual Allowance, which is the amount of pension contributions you’re allowed to receive tax relief on every year. Normally, it’s 100% of your income up to a maximum of £60,000 (2025/26), but it can be less for some high earners.

The Telegraph reports that the level of tax relief received may change as the government is considering capping it at 20%. If you’re a higher- or additional-rate taxpayer, this could mean a 20% or 25% drop in the amount the government effectively gives you towards your pension.

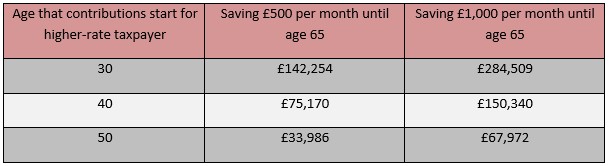

The tables below show how much you could lose if the rebate is capped at 20% if you’re a higher- or additional-rate taxpayer. The figures assume that you’ll retire at 65 and that your pension enjoys 5% investment growth per annum after charges.

Source: the Telegraph

As you can see, depending on the age you start contributing, capping tax relief at the basic rate means you could lose between £33,986 and an eye watering £355,636 by the time you retire at 65.

That said, there has also been speculation in the media that the government may introduce a flat-rate rebate of 30%. While this still reduces the relief that you’ll receive as a higher- or additional-rate taxpayer, it won’t be as severe, and it’ll benefit you if you’re a basic-rate taxpayer.

2. The cost of your pension could rise for your employer

The second way the government may adversely affect your pension is by taxing employers on the contributions they make to your pension.

While your employer has to contribute a minimum 3% to your workplace pension, they might give you more because it’s currently tax free for them. If this changes and your employer has to pay tax on contributions, which will increase costs, you may see your employer reduce contributions to the minimum.

If this happens you may need to increase your contributions to keep your pension on track. A financial planner will be able to help confirm this and explain your options.

Use your tax reliefs before you potentially lose them

If you are a higher- or additional-rate taxpayer, speaking to a financial planner to ensure you maximise the tax relief currently available would probably be a shrewd move.

For example, you might be able to boost contributions before any regulation changes using “carry forward”. This may allow you to boost your tax-efficient contributions by making the most of any unused Annual Allowance from the previous three years.

In addition, a financial planner can ensure sure you’re maximising your pension contributions before the potential changes, which could help you achieve your retirement goals.

If you would like to discuss your pension and any potential tax implications, please email me on a.douglass@grosvenorconsultancy.co.uk or call my office on 01793 766 123. Alternatively call my mobile on 07525 177 046.

While I offer high standards of service and will work with you to ensure any plan is right for you, I’m also a busy mum, so work Mondays and Tuesdays only.

Please note

This article is for information only. Please do not act based on anything you might read in this article. All contents are based on our understanding of HMRC legislation, which is subject to change.

The value of your investment can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance. Your pension income could also be affected the interest rates at the time you take your benefits. Levels, bases of and reliefs from taxation may be subject to change and their value depends on the individual circumstances of the investor.