Figures from the Office for National Statistics show the number of centenarians in the UK reached record levels in 2020, with 15,120 Britons trying to squeeze 100 candles onto their birthday cake.

Interestingly, research by pension specialist Just Group also found that female centenarians outnumbered males by nearly five to one. While it may not be obvious, this could create a financial dilemma for many women.

The reason for this is that most women’s pensions are significantly smaller than men’s. For example, research by the University of Manchester found men aged between 65 and 69 years had average pension pots of £212,000. Women averaged £35,000.

As you can see, this could present financial challenges for women who live to a grand old age. If you’re asking yourself: “how can I secure my financial future?”, there are clever steps that you could take to help ensure it, no matter how long you live for.

Read on to discover three.

1. Boost your pension

Increasing the size of your pension pot could provide a higher income and ensure its longevity. There are several ways you could do this, which we’ll consider now.

Increase contributions

Pension contributions typically receive tax relief. This means that if you’re a basic-rate taxpayer, every £100 you contribute costs you just £80 (2022/23). If you’re a higher-rate or additional-rate taxpayer, a contribution only costs you £60 or £55 respectively.

As you can see, increasing your contributions could offer a significant boost to your pension pot. This is subject to your Annual Allowance, which in 2025/26 is the lower of £60,000 or the amount you earn.

Use “carry forward”

If you have a lump sum such as an inheritance, you may be able to use carry forward to make a larger pension contribution. If so, you can use unspent allowance from the previous three years, potentially allowing you to contribute up to £180,000 in 20225/26 and still receive tax relief.

Contribute more to your workplace scheme

If your employer matches your pension contributions, placing as much money as you can into it is likely to be a shrewd move. With matched contributions you’re effectively doubling your money, which could significantly boost your retirement pot.

Find lost pensions

According to Unbiased, British workers have lost up to 1.6 million pensions with an estimated value of £19.4 billion. If you’ve lost a pension, finding it could help increase your retirement fund.

A financial planner can help with this and provide options. For example, you might want to consider merging it with other pensions to potentially provide greater growth potential.

2. Consider life cover for your spouse

If your pension income will not support your lifestyle after your spouse’s death, you may want to consider protecting their life. This means you’ll receive a lump sum when they die, which might generate additional income for you.

A financial planner can confirm whether this is an appropriate strategy, and locate the most cost-effective life cover.

3. Consider investing your savings

If you intend to use cash savings to boost your pension income, care needs to be taken. This is because the rising cost of living – otherwise known as inflation – could significantly reduce the value of your savings in real terms.

If you use an inflation calculator, you’ll see that you need £184 in March 2022 to have the same spending power as £100 in 2002. In other words, your money needed to grow 84% to keep up with an average inflation rate of 3.1% during the period.

This is half the 6.2% inflation rate reported by the Office for National Statistics for February 2022.

When you then consider the Times reveals the best instant access savings account offered 0.84% in March 2022, you can see how your money could lose ground to inflation in real terms. It also points out that the best fixed-rate bonds, which offer set interest rates for up to five years, offer 1.6%.

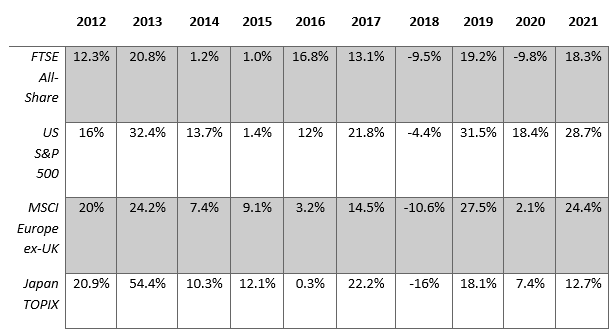

One way you could inflation-proof your money is to invest it, as typically this offers greater growth potential over the long term. Consider the table below, which shows the annual returns of some of the major stock indices over the 10 years to 2021.

Source: JP Morgan, FTSE, MSCI, Refinitiv Datastream, Standard & Poor’s, TOPIX, J.P. Morgan Asset Management. All indices are total returns in local currency, except for MSCI Asia ex-Japan and MSCI EM, which are in US dollars. Past performance is not a reliable indicator of current and future results. Data correct as of 31 January 2022.

As you can see, with one or two exceptions, the stock markets have largely produced annual returns that could help inflation-proof your money. Always remember, past performance is no guarantee of future performance, and you may receive less than your initial investment.

Investing might not only help you generate a better future income for yourself, it could help you do your bit for the planet as well. According to Pension Age, placing your pension or investments into Environmental, Sustainable and Ethical (ESG) funds could be 40 times more powerful in tackling climate change than switching to a renewable energy provider.

Get in touch

If you would like to discuss how you could ensure your long-term financial security, your wider wealth or investing in ESG funds, please contact me. I can be reached by emailing a.douglass@grosvenorconsultancy.co.uk or by calling my office on 01793 766 123.

Alternatively, call my mobile on 07525 177 046. Please note that while I offer high standards of service and ensure any plan is right for you, I’m also a busy mum, so work Mondays and Tuesdays only.

Please note

This article is for information only. Please do not act based on anything you might read in this article. All contents are based on our understanding of HMRC legislation, which is subject to change.

The value of your investment can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.

A pension is a long-term investment. The fund value may fluctuate and can go down, which would have an impact on the level of pension benefits available. Your pension income could also be affected by the interest rates at the time you take your benefits. The tax implications of pension withdrawals will be based on your individual circumstances, tax legislation and regulation, which are subject to change in the future.